Table of Contents

ToggleWhat is a CRIF Credit Report?

A CRIF (Centre for Research in International Finance) Credit Report is an overview report of your credit history. It is created by CRIF High Mark, a credit bureau in India. This report shows your financial behaviour which includes borrowing habits, loan and credit card details, repayment history. It also includes a credit score—a three-digit number (ranging from 300 to 900) that represents how good you are at managing credit. A higher score means you are financially responsible and have better chances of getting a personal loan or credit card approved.

How CRIF Credit Reports Work

CRIF Credit Reports are generated using data provided by banks, financial institutions, and other lenders. Here’s how the process works:

- Data Collection: Lenders share information about your loans, credit cards, repayment patterns, and defaults.

- Data Processing: CRIF High Mark compiles and processes this information to create your credit report.

- Credit Scoring: Based on the report data, a credit score is calculated. Scores typically range from 300 to 900, with higher scores indicating better creditworthiness.

- Report Access: Lenders can access your report when you apply for credit, helping them evaluate your ability to repay.

This report not only aids lenders but also empowers you to understand your financial standing and take corrective measures if needed.

How to Obtain Your CRIF Credit Report?

Getting your CRIF Credit Report is a straightforward process:

- Visit the CRIF High Mark website.

- Navigate to the “Get Your Credit Report” section.

- Fill in your personal and financial details, such as PAN number, date of birth, and email address.

- Verify your identity using an OTP sent to your registered mobile number or email.

- Make the payment if applicable and download your report.

CRIF Credit Report vs. CIBIL Credit Report

Features | CRIF | CIBIL |

Credit Score | 300-900 | 300-900 |

Provider | CRIF HIgh Mark | TransUnion CIBIL |

Access to Report | Free once a year | Free once a year |

Market Size | Smaller but growing | Largest market share |

Both reports are reliable, and choosing one depends on your lender’s preference or your personal needs.

Also Read: How to Choose Best Personal Loan Lender – Top 8 Reasons

Factors Impacting Your CRIF Credit Score

- Payment History: Repayment of loans and credit bills on time boosts your credit score.

- Credit Utilization: Maintaining a low credit utilization ratio (below 30%) positively impacts your score.

- Length of Credit History: A longer credit history with positive records indicates stability.

- Credit Mix: A balanced mix of secured and unsecured loans enhances your score.

- Credit Inquiries: Frequent loan or credit card applications can lower your score due to hard inquiries.

- Defaults: Missed payments or defaults negatively affect your score.

Why is the CRIF Credit Report Important?

A CRIF Credit Report plays a vital role in your financial journey. It helps:

- Lenders assess your creditworthiness for loan approvals.

- Determine interest rates and loan terms based on your score.

- Identify potential errors or discrepancies in your financial records.

- Empower you to take control of your financial health.

Maintaining a strong CRIF Credit Report ensures smoother access to credit when needed.

Benefits of Having a Good CRIF Credit Report

- Easier Loan Approvals: A high score makes you a preferred borrower.

- Lower Interest Rates: Lenders offer better rates to individuals with good credit scores.

- Higher Credit Limits: Financial institutions are more likely to extend higher limits.

- Improved Negotiation Power: A strong credit profile gives you leverage during loan negotiations.

How to Improve Your CRIF Credit Report?

- Pay Dues on Time: Always pay EMIs and credit card bills promptly.

- Limit Credit Applications: Avoid frequent hard inquiries by limiting loan or credit card applications.

- Monitor Credit Utilization: Keep your utilization ratio below 30%.

- Check for Errors: Regularly review your report and dispute inaccuracies.

- Diversify Credit: Maintain a mix of secured and unsecured credit.

Common Mistakes in CRIF Credit Reports

Mistakes in credit reports are more common than you’d think—and they can impact your financial life big time! Let’s break it down:

- Incorrect Personal Details: Errors in your name or PAN can lead to mismatches.

- Unrecorded Payments: Missed updates on paid dues can lower your score.

- Duplicate Accounts: Errors like duplicate loan entries can affect your score.

- Identity Theft: Fraudulent transactions under your name can harm your report.

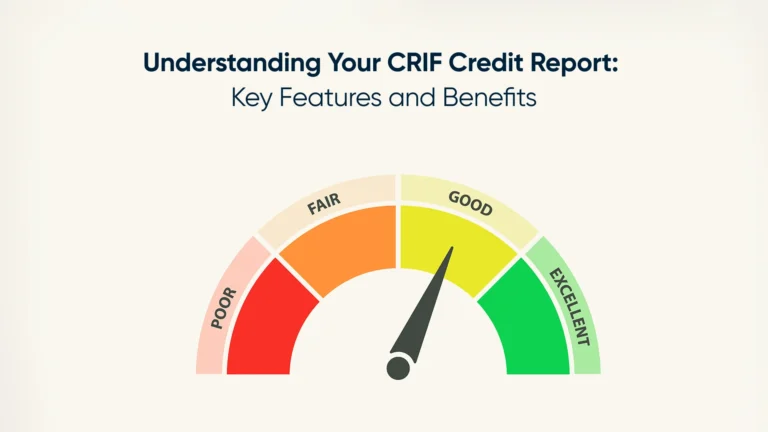

Understanding CRIF Credit Report Ratings

Here’s a simple table format to understand CRIF credit report ratings:

Rating | Score Range | Meaning |

Excellent | 750 & above | Excellent Credit History and highly eligible for financial products and favourable interest rates |

Good | 700-749 | Credit History is strong, and you are reliable |

Average | 650-699 | May face slightly higher interest rates, but obtaining credit is still accessible |

Fair | 600-649 | Loan approval becomes challenging and gets loan with higher interest rates |

Poor | Below 600 | Getting loan and credit is difficult and need to improve financial habits |

CRIF Credit Report for Loan and Credit Approval

A good CRIF score shows you’re responsible with your finances, which increases your chances of getting approved for loans or credit cards with better terms. On the other hand, if your report has some red flags, like late payments or high debt, it could hurt your approval chances.

The good news is, you can always check your CRIF credit report and score to see where you stand. If you spot any mistakes, you can raise a dispute to get them fixed. Keeping your credit in check can help you secure better loan deals, lower interest rates, and make your financial journey a whole lot smoother. So, before applying for that loan or credit card, it’s always a good idea to take a quick look at your CRIF report!

How to Dispute Errors in Your CRIF Credit Report?

Here’s how you can raise dispute for errors in your CRIF Credit Report:

- Check for mistakes and inaccuracies in your report first.

- Visit Official Website: https://www.crifhighmark.com/raise-a-dispute

- Navigate on “My report” and select “Raise a query” tab

- Choose the credit report for which you want to raise a dispute and click on “Proceed.”

- Choose the account or information you wish to modify and click “Submit” to initiate the dispute.

- Monitor the resolution process and ensure corrections are made.

Conclusion: Importance of Maintaining a Good CRIF Credit Report

In conclusion, maintaining a good CRIF credit report is like your financial reputation—lenders, banks, and even some employers rely on it to gauge your trustworthiness. By keeping track of your credit score, paying bills on time, and managing debt responsibly, you’re setting yourself up for easier access to loans, better interest rates, and a stronger financial future. So, take a little time to review your credit report regularly, spot any errors, and keep those good habits going. It’s an investment in your financial health that can pay off big down the road.

Also Read: CRIF Full Form: Meaning, CIBIL & CRIF Score Differences

Frequently Asked Questions

What Is A CRIF Credit Report And Why Is It Important?

It’s a detailed summary of your credit history. Lenders use it to evaluate your creditworthiness before approving loans or credit.

How Do CRIF Credit Reports Differ From Other Credit Reports?

CRIF provides unique insights and accuracy in analyzing your credit data compared to other bureaus, with lenders often relying on it for approvals.

How Can I Check My CRIF Credit Report?

Visit the CRIF website, provide basic details, and download your report. Some banks and apps also offer it for free.

What Factors Affect My CRIF Credit Score?

Payment history, credit utilization, loan types, credit inquiries, and repayment tenure all impact your CRIF credit score.

How Can I Improve My CRIF Credit Report?

Pay dues on time, reduce outstanding debt, limit credit inquiries, and maintain a healthy credit mix to improve your score.

Can Errors In My CRIF Credit Report Affect My Loan Application?

Yes, inaccuracies can lower your score or show false defaults, leading to rejections. Correct errors promptly to avoid issues.

How Do Lenders Use CRIF Credit Reports For Approval?

Lenders analyze your credit report to assess repayment ability, credit habits, and risk before approving loans or credit cards.