Lenders place a high priority on your ability to repay the borrowed amount when you apply for a loan, mortgage, or credit card. They closely assess your creditworthiness, considering your past debt management practices and your ability to take on new financial responsibilities. One of the common ways that lenders determine this dependability is by looking at the “5 C’s of Credit.” Gaining an understanding of these five essential pillars will greatly improve your creditworthiness and raise your chances of being approved for personal loans. We’ll go into detail on each of these Cs in this article, giving you a guide on how you need to improve your credit and get the credit you require.

Table of Contents

ToggleUnderstanding the 5 C’s of Credit

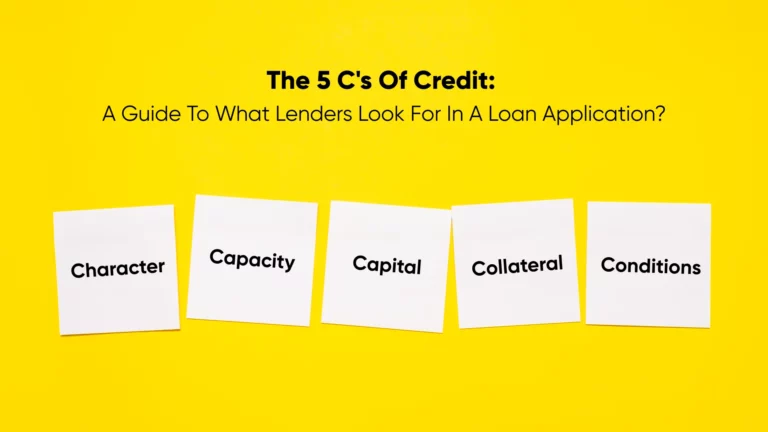

For anyone looking to borrow money, it is essential to understand the five Cs of credit. These Cs—Character, Capacity, Capital, Collateral, and Conditions—are what lenders use to decide whether to lend you money and on what terms. While capacity assesses your ability to repay, character considers your credit history. Collateral is what you offer as security, Capital is what you have invested, and Conditions consider external factors. You may improve your credit score, manage your money more skillfully, and raise your chances of obtaining a loan with favorable terms by being aware of each of these factors. With this knowledge, you can confidently handle the borrowing procedure.

What are the 5 C’s of Credit in Loan?

Character:

Character, one of the critical aspects of the 5 Cs of credit, examines a borrower’s reputation and track record when it comes to repaying debts. Within this category, lenders consider several characteristics, including the borrower’s credit score, payment history, and any prior bankruptcies A good credit score and a consistent history of timely payments demonstrate responsible financial behavior, which in turn enhances the borrower’s credibility in the eyes of lenders. On the other hand, a history of bankruptcies or late payments could worry lenders because it suggests a higher default risk. Thus, to get good loan terms and interest rates, borrowers must have a solid credit history.

Capacity:

An important consideration for determining a borrower’s creditworthiness is capacity. Its main objective is to assess the borrower’s capacity to repay the loan by considering a range of financial factors. To assess a borrower’s ability to manage further financial obligations, lenders look at their income level, employment stability, and past debt obligations. This evaluation helps lenders gauge whether the borrower has enough income to comfortably cover the loan payments without facing financial strain.

Capital:

Capital represents the borrower’s investment in the loan transaction. This includes assets, savings, and investments that can serve as a financial cushion in case of unforeseen circumstances. A higher capital stake indicates a greater commitment to the loan and reduces the lender’s risk. Overall, capacity assessment ensures that borrowers are not overextended financially and have the means to fulfill their repayment responsibilities, thereby reducing the risk of default for lenders.

Collateral:

A vital part of the instant loan process, collateral protects lenders from any losses in the case of borrower default. Collateral is essentially defined as assets pledged by borrowers to provide lenders with a physical form of security for the loan. Borrowers provide lenders assurance that they have a stake in repaying the loan by pledging collateral. Lenders have the right to seize and sell collateral to recover their losses if a borrower fails to meet their repayment obligations and defaults on the loan. Lenders can offer loans with more advantageous terms and cheaper interest rates because collateral gives them a sense of security and assurance. On the other hand, borrowers who guarantee collateral might be eligible for larger loan amounts and higher loan approval rates. To prevent losing their assets, borrowers must, however, be aware of the risks associated with pledging collateral and make sure they can fulfill their repayment commitments.

Conditions:

Conditions are external factors that could affect the borrower’s capacity to pay back the loan. Economic variables like personal loan interest rates, inflation rates, and market conditions may be among these factors. Lenders also consider factors industry-specific conditions and regulatory changes that may affect the borrower’s capacity to fulfill their financial obligations. Lenders analyze how the loan funds are going to be used and modify their lending requirements as necessary. A borrower looking for an urgent personal loan for debt consolidation may not be subject to the same terms as someone seeking a loan for business expansion. Lenders can meet borrower demands while making well-informed judgments about loan approvals, interest rates, and repayment terms. Similarly, borrowers should consider these external factors when applying for a loan to ensure they can comfortably meet their repayment obligations under various conditions.

Also Read: Consolidate your Debt with Personal Loan

Conclusion

To sum up, the 5 C’s of Credit offer lenders a thorough framework for analysing loan applications and determining the creditworthiness of the borrower. People and organisations can increase their chances of obtaining favourable loan terms. Giving the 5 C’s top priority will help you achieve financial success and provide you the ability to make wise borrowing decisions, regardless of how experienced you are as a borrower or if this is your first time exploring the loan process.

Frequently Asked Questions

Which Of The 5 C's Of Credit Requires That A Person Be Trustworthy?

One of the five components of credit – character, requires that an individual behave with integrity when handling money. Lenders evaluate a borrower’s character by looking at things like credit history, payment history, and integrity in fulfilling past obligations.

Can You Explain The Significance Of Character In The Context Of Credit Assessment?

Character is very important when evaluating credit since it shows how trustworthy and honest a borrower is at paying back loans. A strong character makes a borrower more creditworthy and gives lenders trust. This can be shown by a positive credit history and appropriate financial behavior.

What Role Does Collateral Play In Securing A Loan?

Lenders use collateral as security if the borrower defaults. Borrowers give lenders a type of guarantee by pledging assets like real estate, cars, etc. This enables lenders to recover losses by taking possession of and selling the collateral if needed.

How Can Borrowers Improve Their Creditworthiness Based On The 5 C's Of Credit?

To improve their creditworthiness, borrowers should keep up a positive credit record, manage debts responsibly, and be mindful of external conditions that may impact their ability to repay.

Are The 5 C's Of Credit Equally Important, Or Do Lenders Prioritize Certain F actors Over Others?

The type and size of the loan, as well as the unique circumstances of each borrower, may determine which of the five C’s of credit is given priority by the lender when assessing loan applications. Character, capacity, and collateral are typically given a lot of consideration when granting credit.

What Steps Can Individuals Take To Strengthen Their Application In Each Of The 5 C's Areas?

Individuals can strengthen their loan applications by maintaining a strong credit history, improving their income and employment stability, increasing their financial reserves, offering valuable collateral, and demonstrating an understanding of prevailing economic conditions.

Are There Any Common Misconceptions About The 5 C's Of Credit That Borrowers Should Be Aware Of?

One common misconception is that having a high income guarantees loan approval. While income is important, lenders consider various factors, including credit history and collateral. Additionally, borrowers should not overlook the significance of external economic conditions in credit assessment.

In What Ways Do Economic Conditions Impact The Evaluation Of The 5 C's Of Credit By Lenders?

Economic conditions, such as interest rates, inflation, and unemployment rates, can influence a borrower’s capacity to repay a loan. Lenders consider these factors when assessing credit applications and may adjust their lending criteria accordingly.

Are The 5 C’s Of Credit Applicable Only To Personal Loans, Or Do They Extend To Other Types Of Credit As Well?

The 5 C’s of credit apply to various types of credit, including personal loans, mortgages, business loans, and credit cards. Regardless of the type of credit, lenders evaluate borrowers based on their character, capacity, capital, collateral, and conditions.