FICO score model is a relatively new entrant in India compared to other established credit-scoring models. FICO score is mainly built on credit card payment data and India still has a limited credit card user base. As of January 2024, credit card penetration in India stands at 5.5% for its 1.4 Billion population.

This article explains FICO credit scores and how they impact personal loans.

Table of Contents

ToggleWhat is a FICO Credit Score?

The FICO score is a 3-digit score and ranges between 300 – 850. FICO score is a credit score based on one’s credit history. It helps lenders assess borrower’s creditworthiness in a short period. Lenders need a quick way to check the credit history of the borrower. When one applies for a personal loan, lenders consider the FICO score as a quick way to assess whether to approve a loan or not. The FICO score is calculated by an algorithm that considers various factors: History of Repayment (35%), Amounts Owed (30%), Length of Credit History (15%), New Credit (10%), Credit Mix (10%)

To qualify for a personal loan, one needs a FICO score of at least 580. Moreover, if one needs a personal loan at a lower interest rate, they need a FICO score of 800 with a steady income score.

How to Improve Your FICO Credit Score?

There are definitive steps one can take to improve their FICO credit score. Following these steps can improve credit score in a few months to a few weeks, depending on the borrowers’ credit behaviour:

Review Credit Reports: Before improving your credit score, get a copy of your credit report. Your credit report will help you understand which area you need to work on. If there are any errors or unauthorised credit checks, it can impact your credit score. Report them to your credit bureau and get it fixed. This helps improve the credit score.

Pay Bills on Time: Recurring late EMI payments can negatively impact your credit score. Ensure you pay bills on time. Set up automatic payments or reminders to ensure bills are paid on time.

Pay Full Bill Amount: Ensure to pay the full bill amount each month. While there is an option to pay a minimum monthly EMI, it carries forward along with the interest.

Keep Credit Utilisation Ratio Low: Use 30% or less of your available credit. For example: if the credit limit is ₹50,000 aim to utilise around 30% or less of that limit i.e. ₹15,000.

Limit New Credit Applications: Multiple credit applications at the same time, impact the credit score. Avoid or limit new credit applications and only apply for a new one, when necessary.

Keep Your Old Accounts Open: Closing an old account negatively impacts the credit score. A long credit history gives the lender insight into the borrowers’ credit behaviour. Thus, it helps to keep old credit accounts open.

Common Myths About FICO Credit Scores

Myth: Checking Your Fico Score Lowers It

Checking one’s credit score does not lower the score. It is a good practice to regularly check your credit score and keep track of your credit history.

Myth: A Low Credit Score Means Loan Rejection

Low credit score impacts loan application. But doesn’t imply direct rejection. While the chances of loan approval are low, one can still get loans.

Myth: Income Impacts Fico Score

Income is considered as a measurement to pay timely EMI bills. However, it does not impact the FICO score.

Myth: A Good Credit Score Means One Is Rich

Credit score is a measure of risk a borrower has when taking a loan. A low credit score means the individual is a high-risk borrower. Similarly, an individual with a good credit score means they have a good credit history. However, It does not imply whether they are rich or not.

Myth: Getting Married Will Merge One’s Credit Score With Their Spouse

Credit reports stay unique to the individual. If an individual applies for a new loan with their spouse, the credit scores of each one are taken into consideration. However, if a joint loan is taken, the impact of that loan is reflected in both individuals.

Comparing FICO Score with Other Credit Scores

FICO score, CIBIL score and Equifax score are different types of credit scores used by banks and lenders in India. While CIBIL and Equifax are widely used credit scoring models in India, FICO model is a new entrant in India and is used by several lenders. The table below compares FICO score and credit score; CIBIL and Equifax credit scoring models:

Criteria | FICO Score | CIBIL Score | Equifax Score |

Definition | Credit score given by Fair Isaac Corporation (FICO), to represent an individual’s credit history. | CIBIL score is a score calculated by Credit Information Bureau (India) Limited. | Equifax is one of the top credit-scoring bureaus in India & is a joint venture by Equifax and 7 Indian financial institutions. |

Range | Ranges between 300 to 850 | Ranges between 300 to 900 | Ranges between 280 to 850 |

Preferred By | FICO score is mostly used in the U.S. and several International financial institutions. FICO score is relatively new in India and its usage is limited. | CIBIL score is preferred by most Indian banks and financial institutions. | Equifax score is used by several banks and financial institutions, but not as widely as CIBIL. |

Calculation | Score is calculated based on payment history (35%), credit utilization (30%), length of credit history (15%), types of credit used (10%), and recent credit inquiries (10%). | Score is calculated based on credit history, repayment patterns, credit utilization, number of credit inquiries, and loan amounts. | Score is calculated on credit history, existing loans, repayment behaviour, and new credit accounts. |

Score for Loan Approval | FICO score above 670 is preferred for loan approval. | CIBIL score above 750 is preferred for loan approval. | Equifax score above 750 is preferred for loan approval. |

How to Check Your FICO Credit Score

Checking your credit score regularly is a good practice and doesn’t lower your credit score. Here are a few steps, to check your FICO credit score:

Online Banking Portal: You can check your FICO credit score on your online banking portal. It is a quick and convenient way to check your FICO score.

Contact Credit Card Issuer: Several credit card issuers provide the FICO score. You can check your credit card company for the same.

Credit Card Statements: Some credit card issuers mention your FICO score with the credit statements.

Get the FICO score from credit bureaus: Three major credit bureaus offer free credit scores, including the FICO score. The three bureaus are Equifax, Experian, and TransUnion. You can request your FICO score from these credit bureaus.

How is the FICO Credit Score Calculated?

FICO score is determined by considering one’s credit report. FICO credit score is calculated considering the following factors:

- Payment History (35%)

- Amounts Owed (30%)

- Length of credit history (15%)

- New credit (10%)

- Credit mix (10%)

Factors Affecting Your FICO Credit Score

Understanding what affects your FICO score will help you plan your finances better and lead to a better credit history. Factors that affect FICO credit score include:

Payment History (35%): One’s credit history and how quickly one has paid off their loan comprises about 35% of a FICO score. Late payments and missed payments impact the FICO score and lower it.

Amounts Owed (30%): The amount owed in all the credit accounts also impacts the FICO score. The aim should be to keep credit utilisation ratio low. Utilising up to 30% of the credit limit is ideal. For example: if the credit limit is ₹1,00,000, then the credit amount should be utilised up to ₹30,000.

Length of Credit History (15%): The length of one’s credit account affects the FICO score. Old credit accounts and current ones are considered to understand the credit payment history of the individual. A long re-payment history positively impacts their FICO score. It is a good practice to keep old credit accounts open to improve credit history.

New Credit (10%): If one applies for a new line of credit, it leads to a hard enquiry by the lender. If one applies for multiple credits, it signals to the lender that the borrower is heavily reliant on loans and credit. This significantly impacts the credit score and lowers it.

Credit Mix (10%): Credit scoring models prefer a mix of credit like personal loans, credit cards, home loans and so forth. The ability of the individual to successfully manage different lines of credit positively impacts the credit score.

Importance of FICO Credit Score for Personal Loans

The FICO credit score is utilised by lenders to assess the risk factor of the borrower. It is a quick and convenient way for lenders to evaluate the credit history of the borrower. The minimum FICO score required to be eligible for a personal loan is 580. A high FICO score increases loan approval chances. Additionally, a high score of 800 and above offers better loan terms. Lenders offer lower interest rates and flexible payment terms for individuals having high FICO scores. One is also eligible for unsecured loans since a high FICO score implies a low-risk borrower. The loan also gets approved faster with a high FICO score.

Ideal FICO Score for Personal Loans

The FICO score for personal loans ranges between 300 to 850. Lenders refer to the FICO score to quickly assess borrower risk. High credit score increases loan approval and better loan terms. Here are the FICO score range and what each score implies for a personal loan.

FICO Score 800 to 850: Exceptional Rating

Individuals in this range have a good chance of getting loan approval. This score demonstrates the individual has a good credit history and timely repayments of loans and credits.

FICO Score 740 to 799: Very Good Rating

Individuals having FICO scores in this range have an easy time getting loan approval. This score demonstrates positive credit behaviour and has an easier time getting additional credit.

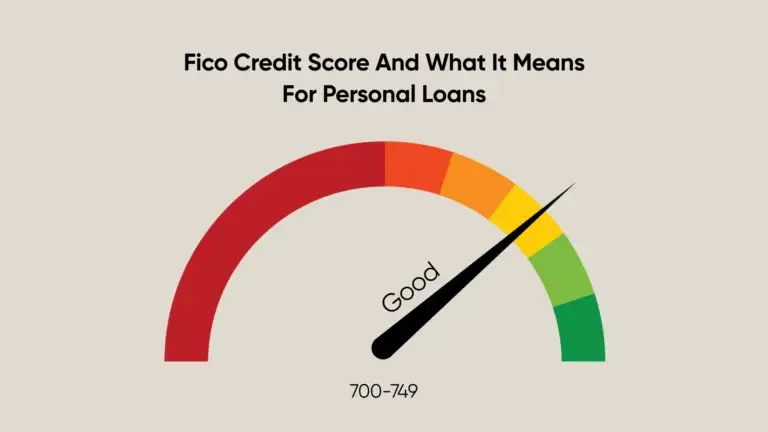

FICO Score 670 to 739: Good Rating

Individuals in this range are low-risk borrowers. This score demonstrates acceptable credit behaviour and most lenders consider this a good rating. Getting a personal loan is fairly easy with this rating.

FICO Score 580 to 699: Fair Rating

Individuals in this range are considered high-risk borrowers. Lenders may not approve their loans easily, since they are high-risk. However, some lenders may approve loans with high interest rates and shorter tenure.

FICO Score Less than 580: Poor Rating

Individuals in this range will have difficulty getting personal loans approved and may face loan rejection. They are considered high-risk borrowers. However, there are a few lenders who look at other factors like employment proof, income proof etc, to check repayment capability and approve loans on that basis.

Conclusion

FICO credit score is fairly new among the credit scoring models in India. There are, however, several top banks and NBFCs that are adopting this credit rating model. Understanding the FICO model will help you build a good score and help you manage your finances. Measures to build good credit remain the same across different credit scoring models. Following credit-building measures like timely EMI payment, clearing old debts, maintaining a low credit utilisation ratio, credit mix and so forth, will ensure you have a good credit score no matter which credit scoring model is used.

Frequently Asked Questions

What Is The Full Form of FICO?

The full form of FICO is Fair Isaac Corporation.

Do Banks Use FICO Scores?

Yes, banks do use FICO scores. However, many lenders still prefer CIBIL scores.

How To Calculate FICO Score?

FICO score is calculated based on one’s payment history (35%), amounts owed (30%), length of credit history (15%), credit mix (20%) and new credit (10%).

What Is A Poor FICO Score?

A FICO score between 300 to 579 is considered poor.

What FICO Score Is Used For Personal Loans?

FICO Score 8 is the most widely used score for personal loans.

How Does A FICO Score Affect Loans?

A higher FICO score increases loan approval. The lender determines the interest rate, loan amount and repayment period on the FICO score of the borrower.

What does the FICO Score Indicate To Lenders?

FICO score is determined by considering factors like payment history, credit mix, length of credit history, amount owed and new credit. Thus, the score helps them determine the creditworthiness of the borrower.

Do FICO Scores Change Over Time?

Yes, FICO scores change over time. FICO score is calculated, based on the credit history at the time of request sent, thus it changes over time.

Are Indian Lenders Using FICO score or CIBIL Score?

Most Indian lenders use CIBIL scores. It is authorised by the Reserve Bank of India (RBI) and regulated by the Securities and Exchange Board of India (SEBI)

What Are The Factors Determining My FICO Score?

Your FICO score is determined by your payment history, amount owed, length of credit history, new credit and credit mix.